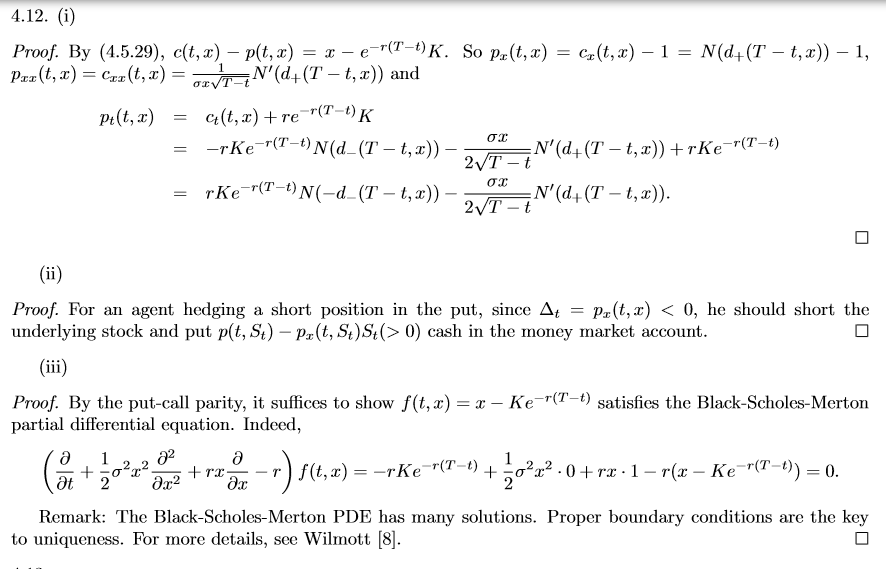

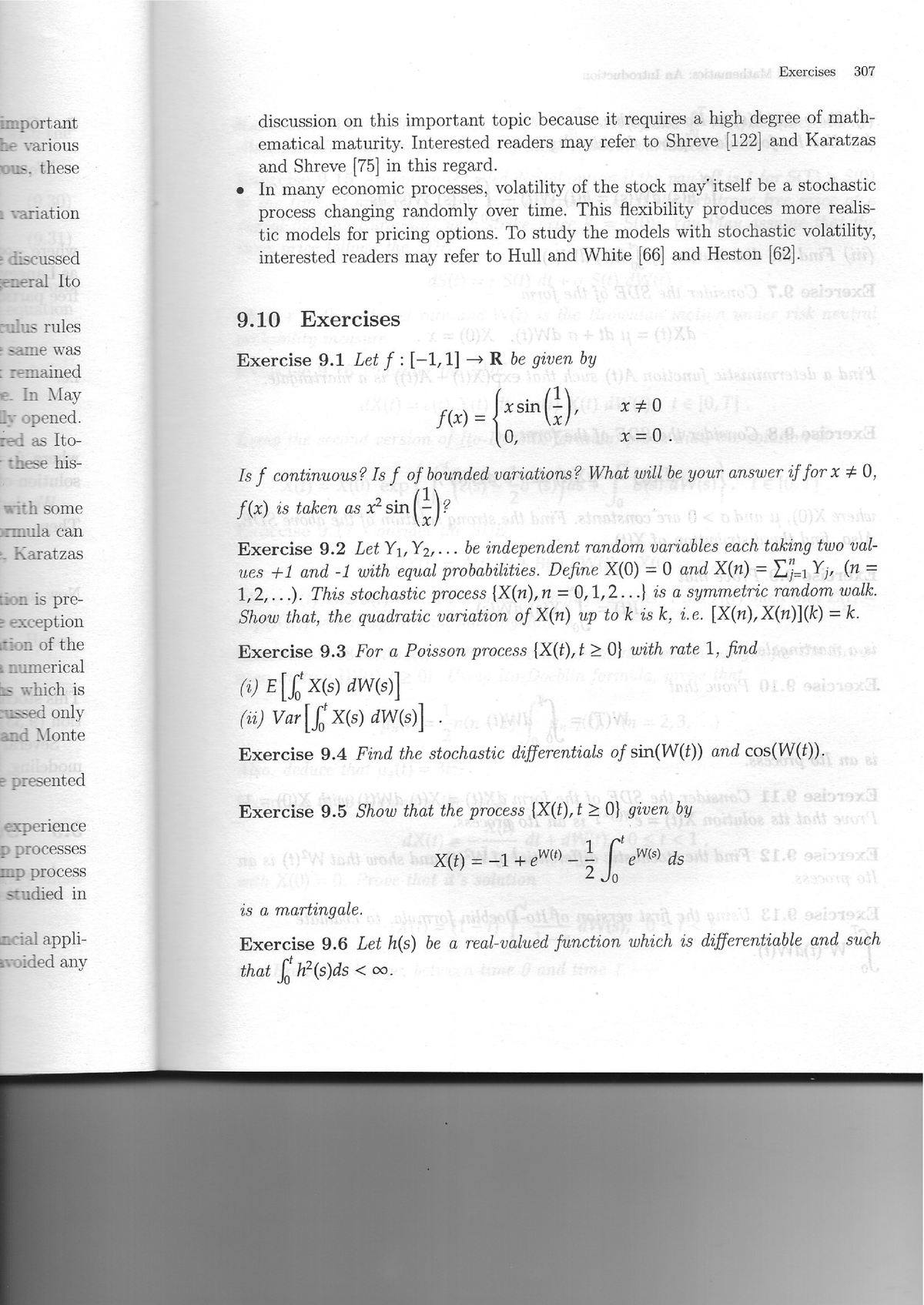

Stochastic Calculus Course

Stochastic Calculus Course - Introduction to the theory of stochastic differential equations oriented towards topics useful in applications. All announcements and course materials will be posted on the 18.676 canvas page. • calculations with brownian motion (stochastic calculus). For now, though, we’ll keep surveying some more ideas from the course: We provide information on duration, material and links to the institutions’ websites. (1st of two courses in. A rapid practical introduction to stochastic calculus intended for the mathemcaics in finance program. Learn or refresh your stochastic calculus with a full lecture, practical examples and 20+ exercises and solutions. It consists of four parts: The main tools of stochastic. (1st of two courses in. Learn or refresh your stochastic calculus with a full lecture, practical examples and 20+ exercises and solutions. The main tools of stochastic calculus (ito's. The course starts with a quick introduction to martingales in discrete time, and then brownian motion and the ito integral are defined carefully. Let's solve some stochastic differential equations! Construction of brownian motion, continuous time martingales, ito integral,. Applications of stochastic models in chemistry, physics, biology, queueing, filtering, and stochastic control, diffusion approximations, brownian motion, stochastic calculus, stochastically. It begins with the definition and properties of brownian motion. We’re going to talk a bit about itô’s formula and give an. This course is a practical introduction to the theory of stochastic calculus, with an emphasis on examples and applications rather than abstract subtleties. Derive and calculate stochastic processes and integrals;. (1st of two courses in. It consists of four parts: Brownian motion and ito calculus as modelign tools for. The main tools of stochastic calculus (ito's. For now, though, we’ll keep surveying some more ideas from the course: Brownian motion, stochastic integrals, and diffusions as solutions of stochastic. We provide information on duration, material and links to the institutions’ websites. Applications of stochastic models in chemistry, physics, biology, queueing, filtering, and stochastic control, diffusion approximations, brownian motion, stochastic calculus, stochastically. The main tools of stochastic. The main topics covered are: It begins with the definition and properties of brownian motion. This series is meant to be a crash course in stochastic calculus targeted towards those who have knowledge of calculus. (1st of two courses in. The main tools of stochastic calculus (ito's. Construction of brownian motion, continuous time martingales, ito integral,. Up to 10% cash back learn or refresh your stochastic calculus with a full lecture, practical examples and 20+ exercises and solutions. Stochastic processes are mathematical models that describe random, uncertain phenomena evolving over time, often used to analyze and predict probabilistic outcomes. This course is a practical introduction to the. It consists of four parts: It begins with the definition and properties of brownian motion. This series is meant to be a crash course in stochastic calculus targeted towards those who have knowledge of calculus. This course is an introduction to stochastic calculus for continuous processes. Transform you career with coursera's online stochastic courses. The main tools of stochastic. This series is meant to be a crash course in stochastic calculus targeted towards those who have knowledge of calculus. Applications of stochastic models in chemistry, physics, biology, queueing, filtering, and stochastic control, diffusion approximations, brownian motion, stochastic calculus, stochastically. Brownian motion and ito calculus as modelign tools for. The course starts with a quick. For now, though, we’ll keep surveying some more ideas from the course: This course is an introduction to stochastic calculus for continuous processes. Derive and calculate stochastic processes and integrals;. Transform you career with coursera's online stochastic courses. The main topics covered are: The main tools of stochastic calculus (ito's. (1st of two courses in. A rapid practical introduction to stochastic calculus intended for the mathemcaics in finance program. This course is a practical introduction to the theory of stochastic calculus, with an emphasis on examples and applications rather than abstract subtleties. For now, though, we’ll keep surveying some more ideas from the. The main tools of stochastic calculus (ito's. This course is an introduction to stochastic calculus for continuous processes. For now, though, we’ll keep surveying some more ideas from the course: This series is meant to be a crash course in stochastic calculus targeted towards those who have knowledge of calculus. • calculations with brownian motion (stochastic calculus). Brownian motion, stochastic integrals, and diffusions as solutions of stochastic. We provide information on duration, material and links to the institutions’ websites. A rapid practical introduction to stochastic calculus intended for the mathemcaics in finance program. • calculations with brownian motion (stochastic calculus). It consists of four parts: Construction of brownian motion, continuous time martingales, ito integral,. All announcements and course materials will be posted on the 18.676 canvas page. The main tools of stochastic. The course starts with a quick introduction to martingales in discrete time, and then brownian motion and the ito integral are defined carefully. Brownian motion, stochastic integrals, and diffusions as solutions of stochastic. Applications of stochastic models in chemistry, physics, biology, queueing, filtering, and stochastic control, diffusion approximations, brownian motion, stochastic calculus, stochastically. It begins with the definition and properties of brownian motion. (1st of two courses in. A rapid practical introduction to stochastic calculus intended for the mathemcaics in finance program. Introduction to the theory of stochastic differential equations oriented towards topics useful in applications. It consists of four parts: This series is meant to be a crash course in stochastic calculus targeted towards those who have knowledge of calculus. Derive and calculate stochastic processes and integrals;. Best online courses that are foundational to stochastic calculus. The main topics covered are: Up to 10% cash back learn or refresh your stochastic calculus with a full lecture, practical examples and 20+ exercises and solutions.

Course Stochastic Calculus for finance Level 2 I

An Introductory Course On Stochastic Calculus PDF Stochastic

Stochastic Calculus The Best Course Available Online

Stochastic Calculus Mastering the Mathmatics of Market

1.1scanned copy Exercise Stochastic calculus Financial Engineering

A First Course in Stochastic Calculus (Pure and Applied

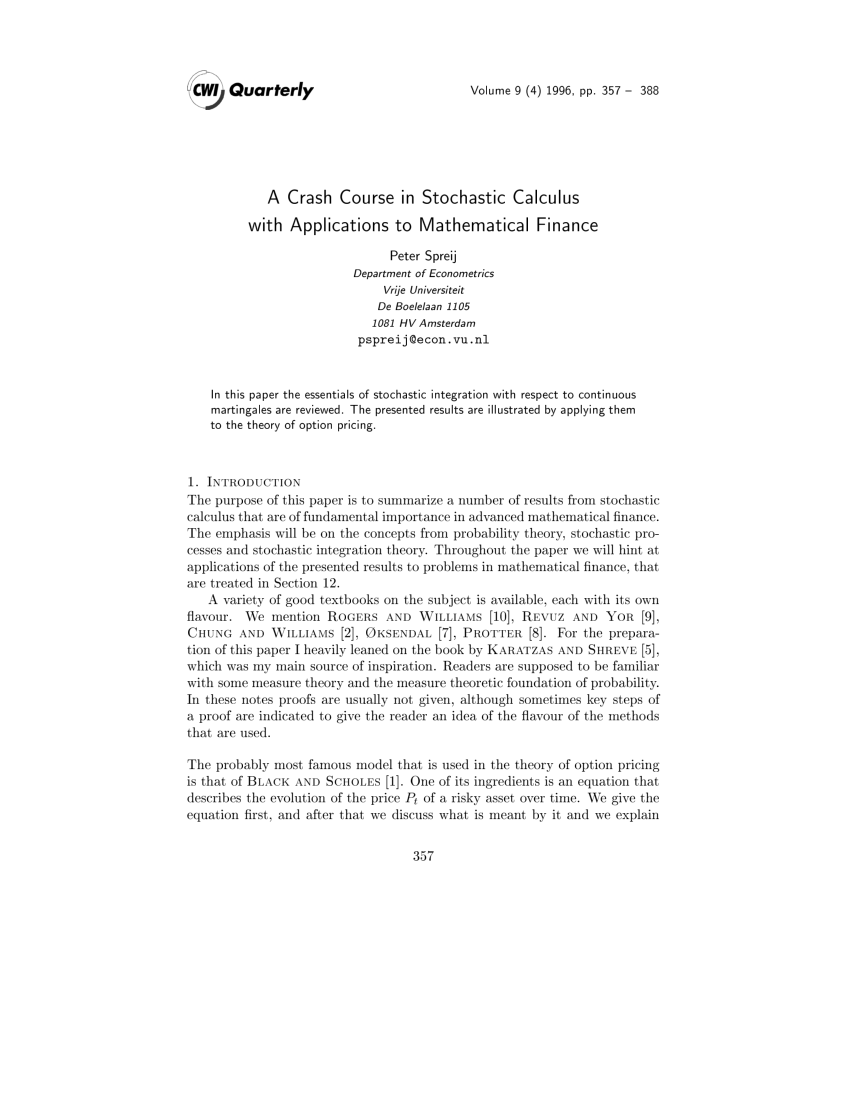

(PDF) A Crash Course in Stochastic Calculus with Applications to

An Introduction to Stochastic Calculus Bounded Rationality

New course Stochastic Calculus with Applications in Finance Center

Stochastic Calculus for finance 45 Studocu

Transform You Career With Coursera's Online Stochastic Courses.

Learn Or Refresh Your Stochastic Calculus With A Full Lecture, Practical Examples And 20+ Exercises And Solutions.

The Course Starts With A Quick Introduction To Martingales In Discrete Time, And Then Brownian Motion And The Ito Integral Are Defined Carefully.

We’re Going To Talk A Bit About Itô’s Formula And Give An.

Related Post: